STP Phase 2 has started! It began on 1st January 2022 and if you are ready and your software is ready, you can begin to report your payroll via this next stage of STP now!

If you aren’t ready, don’t worry, the ATO has provided a blanket deferral to the 1st March 2022. This means that if your software is ready now, you have until 01/03/22 to ensure you are organised and have updated your payroll data to enable a smooth transition to STP Phase 2 reporting.

But how do you know if your software is ready? Most providers would have contacted you by now to explain their plans, but in case you missed their emails, here is a summary of the main providers and whether or not they are ready now:

Have you heard? STP (Single Touch Payroll) is expanding from Phase 1 to, you guessed it, Phase 2. For those who don’t know, STP is a technology that automates the transfer of payroll data from payroll software to government departments, mainly the ATO. STP Phase 2 will see payroll data also being shared with Services Australia, the first in a long list of government departments who will eventually get to see your payroll information (in my opinion). The expansion plan also means that employers will need to update their payroll systems in order to provide much more detail about their payroll at each payroll event (more about that in coming blogs).

This compliance change is happening for better or for worse, so my question is “STP Phase 2, what is it good for?” Absolutely nothing! No, only joking! It turns out that there are quite a few benefits for both employers and employees. This blog will outline those benefits.

Benefits for Employers

Tax File Number Declarations - although you will need to keep copies of your employees' TFN Declarations as part of your employee records, you will no longer need to send them to the ATO. This is because the information will be sent via each pay event through STP.

By nominating an "income type" for employees, you can tell the ATO if you're using concessional reporting for closely held payees or inbound assignees.

If you need to make a Lump Sum E payment (back payments more than 12 months old), you won't need to provide a Lump Sum E letter to your employee as it will be included in the STP report.

If you change software type or an employee's payroll ID number, this will be reported via the STP report. This will help avoid duplicate income statements appearing in employees' myGov accounts.

Data will be shared about some employees with Services Australia (SA). This means that information SA requires from you will be easier to provide e.g. payslips for prior periods.

Because the date and reason for employment cessation will be in the STP report, you will no longer need to complete and provide separation certificates to employees.

Child support deductions and/or garnishees will be reported via STP reducing the need for you to send separate remittance advice to the Child Support Registrar.

Benefits for Employees

Income statements will become more accurate because the ATO will have better visibility of the types of income an employee receives.

If an employee makes an error such as failing to report that he has a study loan debt (resulting in an unwanted tax bill), the ATO will be better placed to rectify the issue sooner rather than later.

If employees have dealings with Services Australia (SA), they will see a more streamlined approach to data capture evolve over time, including:

Prefilled details on claim forms and fewer requests for documentation;

Spending less time on the phone to SA to confirm details;

Receiving SMS or email advice when STP data shows their family income estimate may be too low, they have a new job or their employment details have changed in some way;

Ensuring that they are paid the correct amount from SA, and

Helping SA understand their financial situation if employees need to repay a debt to SA.

STP Phase 2 requires employers and bookkeepers to make major changes to payroll set up which in the interim, may seem onerous and pretty annoying. However, as can be seen above, there are many benefits for both employers and employees that will come from STP Phase 2 in the long run.

Of course, time will tell if these changes will run smoothly or have unwanted side effects. We will all have to wait and see how things play out. In the meantime, for those wanting further information about STP Phase 2, please visit the ATO STP Phase 2 resources page.

In an attempt to protect and improve workers’ retirement savings, the Government announced super reforms “Your Future, Your Super”. This was passed into law on the 24th of June 2021.

As part of these new laws, how you, as an employer, deal with new employees’ super funds and subsequent payment into those funds, has changed.

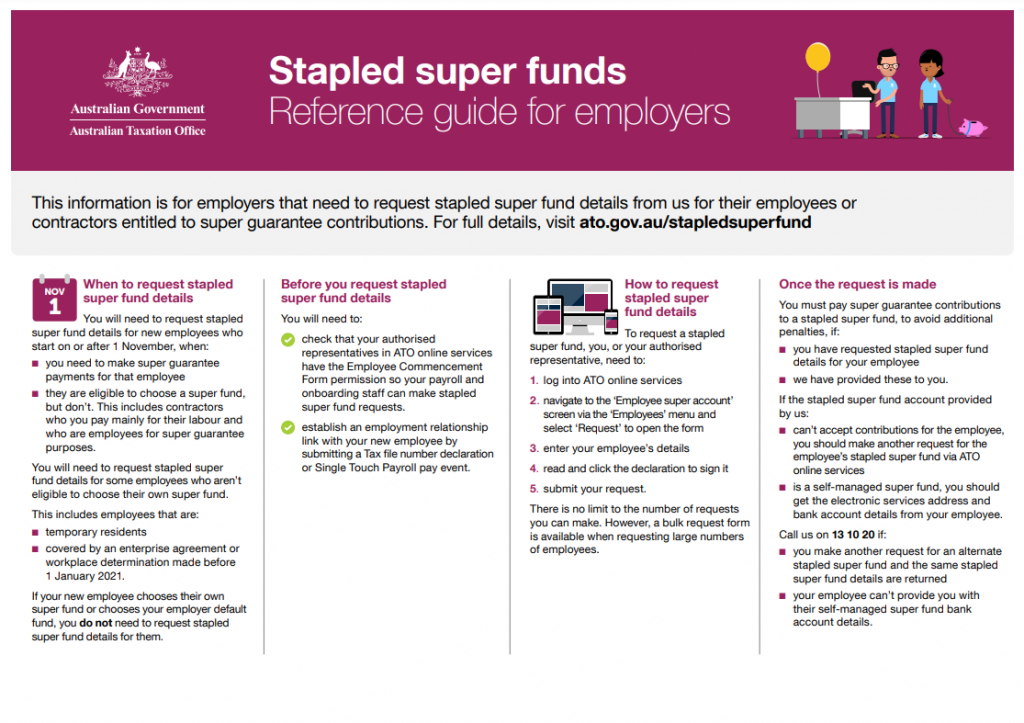

From 1st November 2021, when a new employee starts working for you, you must pay their super into their “Stapled Super Fund” if he/she does not provide you with a choice of fund.

What is a Stapled Super Fund (SSF)?

An SSF is an existing super account that is linked or “stapled” to an employee so that it follows him/her around when he/she changes jobs.

Why do we need Stapled Super Funds?

In the past, it was common for employees to end up with multiple super accounts, especially when employers paid super into their default super funds. Having multiple accounts means that employees are unwittingly paying fees from each account which can add up to a lot of lost retirement savings. From the ATO, “the change aims to reduce account fees by stopping new super accounts being opened each time an employee starts a new job”.

How do you know when you need to use a SSF and how do you do it?

Currently, when a new employee starts working for you, you must provide him/her with a Super Standard Choice Form to complete. The form will provide you with the employee’s super details. If the employee fails to provide these details to you, you must then find out what his/her SSF is and pay super into that fund.

A request for an SSF for your employee is done via Online services for Business (or your Tax/BAS Agent can do it for you). If you cannot access Online Services, you can ring the ATO on 13 10 20 to make the request. When you log into your online account, go to the Business tab, then Employee Super Accounts, then click on “request”. Follow the prompts and you will be provided with the SSF within minutes.

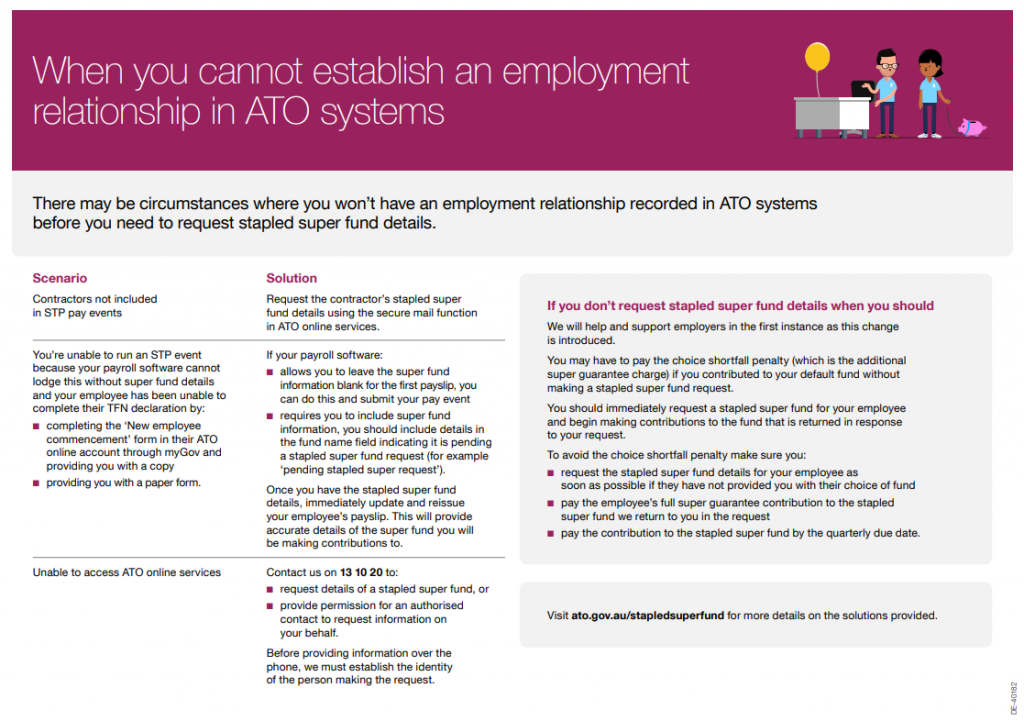

Please note, that you will not be able to make an SSF request until the ATO has confirmed that you are the employee’s employer. This is done via either them receiving the Tax File Number Declaration details or by an STP lodgement event.

How is a SSF determined by the ATO?

The ATO will find the fund that has had the most recent contribution paid into it. This will become the employee’s SSF.

What if a SSF is not provided by the ATO?

If this happens and your employee has still not provided his/her super details, you may make payments into your default super fund.

What happens if the SSF rejects the payment?

If this happens, the ATO recommends that you make another request. If the same SSF is provided, then you must call the ATO on 13 10 20 for assistance.

Is there a transition period?

Yes! The ATO is providing a transition period. This will be between 01/11/2021 and 31/10/2022. After this period has ended, the ATO may apply penalties should you fail to comply with the Stapled Super Fund rules.

Summary – see our infographic below (free to download)

Stapled Super Funds begin on 1st November, 2021.

Only request SSF for employees who do not provide their super details to you.

SSF requests are done via Online Services for Business or your Tax/BAS Agent can make the requests on your behalf.

If an SSF does not exist, you may make super payments for the employee into your default super fund.

The minimum super guarantee (SG) percentage employers are required to pay, is set to increase to 10% on 1st July 2021. This should be considered in part, as a wage increase, and therefore an increase to the overall payroll budget.

There is a further sting in the tail to come for employers! The proportion of wages that must be contributed to employees’ superannuation, is legislated to increase half a percent a year, before reaching a final value of 12% by the 2025/26 FY. See the table below which outlines the rate increase schedule.

PERIOD

GENERAL SUPER GUARANTEE (%)

SUPER GUARANTEE (%) FOR NORFOLK ISLAND (transitional Rate) (from 1 July 2016)

1 July 2002 – 30 June 2013

9

0

1 July 2013 – 30 June 2014

9.25

0

1 July 2014 – 30 June 2015

9.5

0

1 July 2015 – 30 June 2016

9.5

0

1 July 2016 – 30 June 2017

9.5

1

1 July 2017 – 30 June 2018

9.5

2

1 July 2018 – 30 June 2019

9.5

3

1 July 2019 – 30 June 2020

9.5

4

1 July 2020 – 30 June 2021

9.5

5

1 July 2021 – 30 June 2022

10

6

1 July 2022 – 30 June 2023

10.5

7

1 July 2023 – 30 June 2024

11

8

1 July 2024 – 30 June 2025

11.5

9

1 July 2025 – 30 June 2026

12

10

1 July 2026 – 30 June 2027

12

11

1 July 2027 – 30 June 2028 and onwards

12

12

What This Means for Your Small Business

Your payroll budget will increase by 0.5%, per employee, every year until the 2025/26 FY.

An employee on a minimum award wage cannot be paid less than the minimum rate already being paid, therefore the SG at 10% is to be calculated on top of, and without reduction to, the original base amount.

Another factor to consider is if the employment agreement or other industrial relations instrument permits it, the components of an employee’s salary package can be altered to increase the SG to 10% and reduce the gross pay (before tax). This means that your employee’s take-home pay will be less than it is now and will continue to decrease each year until 2025. If this scenario affects you and your employees, we recommend that you review the appropriate agreements and seek HR advicebefore 1 July 2021.

If you use an accounting software package, you won’t need to make any adjustments for the SG increase in your payroll – the developers will do that for you. If you process payroll manually, however, you will need to remember to change the percentage from 9.5 to 10 (and again by 0.5 % each year until you reach 12 % in 2025). Remember, if you don’t pay the correct rate of SG into your employees’ super accounts by the quarterly due date, you will have to pay the Superannuation Guarantee Charge (SGC).

With regards to “when” the rate rise should be applied to your payroll, the rule is that it is applicable to any payments made on or after 1 July 2021 – this is regardless of the period in which the services were performed by the employee.

Managing your Payroll Budget & Cash Flow

Every employer’s obligation to pay superannuation will increase as of 1st July 2021 – there is no escaping this change. This is an increased cost to your business that must be considered for cash flow and budgeting purposes.

With the increases to compulsory super contributions coming out of the same business budget as wages, and all other on-costs such as workers compensation, payroll tax, PAYG, and superannuation, you need to be prepared. All future SG increases need to be built into a business budget and cash flow forecast to be considered part of wage increases over time. We recommend that you assess the total employment costs of your business and add a percentage on top of the total costs to cover not just the rise in superannuation, but also any miscellaneous expenses and unforeseen blow-outs. The best practice is that it is better to overestimate than underestimate. Accurate and up-to-date financial records will help a business manage cash flow.

By regularly reviewing your budget and cash flow forecast, you, your bookkeeper, and your Tax Agent can address financial problems immediately. By doing this, you will be empowered to make important and necessary decisions for your business when they are required.

The Fair Work Act 2009 was updated on 26th March 2021 to reflect new workplace rights and obligations for casual employees. One of the main changes to the Act was the requirement for employers to provide their casual staff with a Casual Employment Information Statement. The statement brings to light several aspects of casual employment centered around “casual conversion”. So what is casual conversion and how will affect employers in Australia?

Casual conversion is when a casual employee moves to permanent part-time or full-time employment. The recent changes to the Fair Work Act enforce new casual conversion rules for employers. Some rules affect large employers, while others affect small employers (those with 15 or fewer employees).

If you are a large employer, you must offer your casual employee the opportunity to move to permanent positions when/if s/he:

has worked for you for 12 months

has worked a regular pattern of hours for at least the previous 6 months

could continue to work the same hours (or more hours) as a part or full-time employee without too much disruption to himself or the workplace

You do not have to offer casual conversion if you have reasonable grounds to do so. These may include the following:

the employee’s position will cease within 12 months

the employee’s hours will be significantly reduced

the times and/or the days the work is to be performed will be significantly changed and those changes cannot be accommodated by the employee’s availability to work

making the offer would not comply with a State or Territory law

Please note, however, even if you have decided not to offer casual conversion to your staff initially, this does not mean that they cannot apply for it at a later date.

If you are a small employer, you are less likely to be affected by these new casual conversion rules. However, please note that this does not stop your casual employee from requesting conversion. If this occurs, you must act accordingly and attempt to accommodate the employee’s wishes.

If the employer decides not to make an offer for casual conversion, he must do so in writing as per the Fair Work website. However, I would say that it is best practice to ensure that all communication with your employees about changes to their employment, is in writing. So, if you are going to make an offer for conversion or decline an offer, always put this in writing and file the document with the employee’s records.

If you need further information about casual conversion, please visit the Fair Work website.

Employers now have more incentive to employ workers under 35! The JobMaker Hiring credit legislation has now been passed into law! This credit was part of the 2020-21 Budget, which will operate until 6 October 2022. It is designed to improve the prospects of young individuals getting employment following the devastating impact of COVID-19 on the labour market.

Commencement

The scheme will be backdated to commence on 7 October 2020 and provide eligible employers with the following payments for up to 12 months for new jobs created for which they hire the following young workers:

• $200 a week for hiring a worker aged 16 to 29 for at least 20 hours a week and

• $100 a week for those aged 30 to 35.

Although the scheme is slated to run for just 12 months, that period is the hiring period – not the payment period. Eligible employers who hire an eligible employee as late as the last day of the scheme (6 October 2021), may be eligible for hiring credits for the subsequent 12 months until 6 October 2022.

Employer Eligibility

As an employer, you will be deemed eligible for JobMaker if the following criteria are met:

for the first 6 months of JobMaker, you have hired additional eligible employees (minimum of one additional employee). This is determined by a headcount as at 30 September 2020 and the payroll of the business for the reporting period, as compared to the three-months to 30 September 2020.

have an ABN,

are registered for PAYG withholding,

are up-to-date with lodgement obligations for the previous 2 years (including BAS and income tax returns) and

are reporting payroll through STP

You will not be deemed eligible if any of the following apply:

you are claiming JobKeeper for your business,

you have entities in liquidation or who have entered bankruptcy

your entity is a commonwealth, state, and local government agency (and entities wholly owned by these agencies)

you are subject to the major bank levy

your business is a sovereign entity (except those who are resident Australian entities owned by a sovereign entity.

Employee Eligibility

Employees will be eligible if they:

commenced employment between 7 October 2020 and 6 October 2021

were aged between 16 and 35 years at the time they commenced employment

have worked an average of 20-hours a week for each whole week the individual was employed by the qualifying entity during the JobMaker period.

Additionally, the worker must have met the pre-employment condition which requires that for at least 28 of the 84 days (i.e. for 4 out of 12 weeks) immediately BEFORE the commencement of employment of the individual, the individual was receiving one of the following payments:

parenting payment

youth allowance (except if the individual was receiving this payment on the basis that they were undertaking full time study or was a new apprentice) or

JobSeeker payment.

We note that the new worker must be in a genuine employment relationship. For example, ‘non-arms length’ employees will not be considered eligible employees. This includes family members of a family business, directors of a company and shareholders of a company.

A summary of the above can be downloaded here – this a nifty fact sheet from the ATO. Also from the ATO, is this useful JHC payment calculator. Further fact sheets and information can be found here on this ATO page.

If you have hired new employees from October 2020 or are planning to do so in the next 12 months and are interested in the JobMaker Hiring Credit program, please get in touch with us for further information and assistance.

A new legislative instrument has been released which has extended the services BAS Agents can provide to clients in relation to the super guarantee charge (SGC). BAS Agents have been able to assist clients with superannuation tasks for approximately 2 years now, but this instrument allows them to do more and be of greater benefit to clients.

BAS Agents can currently offer superannuation services to clients like processing, advising upon and lodging monthly/quarterly superannuation guarantee data. The Tax Agent Services (Specified BAS Services Services No. 2) Instrument 2020, as it is known, will allow BAS Agents to expand upon these services to include the following tasks in relation to SGC:

Act as an authorised contact on behalf of clients with the ATO in relation to SGC accounts, payment arrangements, penalty remissions, super audit and/or review activity;

Advising clients when the superannuation guarantee (SGC) charge applies and why;

Advising clients about offsetting late payments of superannuation contributions against the SGC;

Completing the late payment offset election section of the SGC statement;

Acting on behalf of clients in relation to lodging the SGC statement.

The instrument will also allow BAS Agents to view and access superannuation guarantee and SGC accounts in online services.

If you are a BAS Agent and would like to read the detail of the new instrument, here is the link to the Explanatory Statement.

The new legislation means that we can now assist clients with superannuation services on a much higher level and therefore provide more value than before. We have added these new services to our services page where you can also view other services we provide.

If you would like to find out more about the superannuation guarantee charge, go to this ATO webpage.

As part of the economic stimulus triggered by the Corona Virus pandemic, the Federal Government has introduced the “Boosting Cash flow for Employers” measure or as we like to call it, the PAYGW Boost Credit. This measure promises to “refund” the PAYG withholding reported on the BAS or IAS by employers back into their integrated client accounts (ICA) as an offset against any existing BAS/IAS debt. To be clear, this is not a supply of cash to employers into their banks. This is simply crediting PAYGW back into the ICA to effectively reduce BAS/IAS debt. The only time an employer will see any cash is when a refund is created because the PAYGW credit is more than the whole activity statement debt. So who gets these payments, how much do they get and how do they get it? Read on to find out!

WHO IS ELIGIBLE?

Businesses will be eligible for this stimulus measure if they:

Held an ABN on 12 March 2020 and continue to be active

Are a small or medium business including NFP, sole trader, partnership, company and trust entities.

Have an aggregated turnover under $50M

Have made payments from which they have been required to withhold (even if this a zero amount). Such payments may include salary and wages, director’s fees, eligible termination payments, compensation payments and withholding from contractor fees.

Have made GST taxable, GST free or input taxed sales in a previous tax period since 1 July 2018 and lodged a relevant BAS on or before 12 March 2020.

HOW MUCH IS PAID?

PAYG withholding amounts will be credited back to the integrated client account (ICA) of between $20K and $50K. These credits are not income and as such will not be taxed. The do not have to be repaid ever. The good thing is that the PAYG withholding you report on your BAS will still be tax deductible. Note, if you have a tax debt on your ICA, the credit boost amount will simply pay down that debt.

HOW IS IT PAID?

These credits will be applied in two stages to integrated client accounts after 28th April 2020 and after the March 2020 quarter or monthly BAS is lodged. You do not have to apply for this measure, AND you do not receive any actual cash – this is credit only, not cash paid to your bank. The second stage credit will be applied in quarter 1 of 2020-21.

HOW DO THE PAYMENTS WORK?

Put simply, there are 2 payment stages for this measure. The first stage is a payment of up to $50K based on the amount of PAYGW reported on the March 2020 BAS. Examples below:

Quarterly Lodgers

If your March 2020 BAS shows a PAYGW amount of $12,000, this amount will be credited back to your ICA. In your June 2020 BAS, if a $14,000 PAYGW is reported, then this will also be sent back to the ICA. So far, a total of $26,000 has been credited. This is the first stage amount. The second stage amount will be the same as the first one i.e. $26,000 and will be credited to your ICA split evenly across June to September 2020.

Monthly Lodgers

If your March 2020 BAS shows a PAYGW amount of $12,000, this amount is multiplied by 3 (to take up amounts for January and February 2020) to give you a credit of $36,000. April, May and June 2020 BAS’s will continue to be lodged which may or may not total more than $50K. For this example, let’s say April was $10,000, May was $8,000 and June was $6,000. This will be a total PAYGW of $60,000. As the first stage payable can be no more than $50K, then $50K is all that will be credited to your ICA. The second stage payment will also be $50K.

What if my PAYGW is less than $10K or zero in my March 2020 BAS?

In this case, you will be credited $10K in the first stage of credits and another $10K in the second stage for a total of $20K.

Coronavirus (COVID-19) has brought with it great uncertainty and worry amongst the general population, not the least of these, employers and staff. There are many unknowns relating to how to manoeuvre in these difficult times as an employer, especially in terms of ensuring staff are treated correctly and fairly. Recently, Fairwork released some direction for employers on their website. We advise you read the bulk of the details on their page yourself but we do provide a “taste” of the information provided below.

My employee (or his family member) has Coronavirus. What now?

You must direct the employee not to come to work and to only return when s/he has been given medical clearance. If the employee is part or full time, s/he will be able to take paid personal/carers leave. Casual workers will need to take unpaid leave given they do not receive leave entitlements. Workers refusing to use their leave entitlements are not required to be paid. You can ask the employee for evidence of the illness or emergency i.e. doctor’s certificate if required.

My employee wants to stay home to avoid contact with others.

In this case, you need to discuss this with the staff member and come to an agreement that suits you both. If working from home is an option and your staff member agrees to do so, then make arrangements together to ensure this can occur easily and smoothly. If the employee cannot work from home, then you must decide if paid or unpaid leave will be provided. Where an employee refuses to take paid leave (where it is available), then that employee cannot be paid.

I want to tell my employee/s to stay home.

From Fairwork: ” Under workplace health and safety laws, employers must ensure the health and safety of their workers and others at the workplace as far as is reasonably practicable. ” If you believe that it would be best to instruct your staff to stay home due to possible risks from COVID-19, then you certainly can do so. You can organise a “work-from-home” scenario where possible or if not possible, you can direct staff to remain off site but you must be aware as per Fairwork ” where an employer directs a full-time or part-time employee not to work due to workplace health and safety risks but the employee is ready, willing and able to work, the employee is generally entitled to be paid while the direction applies”, and also “standing down employees without pay is not generally available due to a deterioration of business conditions or because an employee has the coronavirus.”

I want to direct staff not to travel.

While you can direct your employees not to travel for work-related events, meetings etc because you want to reduce the risks associated with COVID-19 at your workplace, you cannot ask them to cancel personal travel/trips.

So, in summary, you need to ensure your workplace is safe and you can do this by keeping unwell employees at home and/or all staff at home if required. If your business is structured in such a way that working from home is possible, then certainly bring that to the table and discuss with staff how best to handle that scenario. Part and full time staff should take personal leave if affected by the virus or unpaid leave if they prefer. Similarly, if staff unaffected by COVID-19 request to remain at home and also cannot work from home, they must opt to take annual or unpaid leave. If you direct staff to stay home and there isn’t any evidence that they have been affected by COVID-19, that is, they are well and able to work, then you must continue to pay them as normal. To read the full list of instructions provided by Fairwork, download their factsheet below.

Back in May 2018, the first iteration of a law for an amnesty on unpaid historical superannuation was announced, but due to the calling of the Federal election at the time, it did not pass. A second iteration of the law, known as the “Recovering Unpaid Superannuation” Bill, was launched in September 2019. This second attempt was given the green light by the Senate Economics Legislation Committee in November 2019. The Bill is yet to receive royal assent, but if achieved, will mean that many employers will be given the chance to self-report their non-compliance and avoid the usual penalties as a reward.

What does the new Bill include?

The second iteration of the Bill to recover unpaid super includes the following:

The period of historical reporting is from 1 July 1992 to 31 March 2018.

The amnesty period will be for 6 months from the date of royal assent.

Employers must self-report to be eligible to partake in the amnesty.

Payments of super made during the amnesty will be tax deductible (note, usually late super payments are not tax deductible).

Administration fees associated with reporting later super to the ATO will be waived.

Interest charges will still apply.

But will it pass?

While the recent thumbs up by the Senate Committee is a step closer to the Bill being passed, there is still a way to go mainly because Labor Senators don’t agree with the Bill. They cite that this will give non-compliant employers an unfair advantage over employers who are doing the right thing. They don’t agree that the payments should be tax deductible or that fees be waived as this sends the message that being non-compliant is “okay” and will be forgiven, even rewarded. Further to this, those employers who usually pay on time but who may err occasionally, will still be subject to all super guarantee penalties and will not enjoy any tax deductions given the amnesty does not apply to any pay period post 1 January 2018. Labor do not support the Bill due to it giving rise to this unfair playing field. They believe the Bill rewards those employers who have been non-compliant for breaking the law.

We aren’t sure what will happen, but given Parliament will not sit now until February next year (2020), nothing will go ahead until then. If the Bill is passed, we will be sure to let you know and also how we can assist you if you are an employer who would like to take advantage of the amnesty. Please note, we certainly won’t cast any judgement on you if you are in this predicament and you come to us for help. While Labor has a point, we are in favour of any vehicle that will put money that is owed to employees back in their pockets – after all, it is their money! Watch this space – we’ll update this blog if/when the Bill is passed.

Update! SG Amnesty Bill passes Parliament so it is definitely a YES!

As of 24th February 2020, the “Recovering Unpaid Superannuation” Bill 2019 has been passed in both houses and is awaiting royal assent. At that point, the amnesty period will start from 24th May 2018 and end six months from the date royal assent is received. Employers will be able to self-disclose non-paid historical superannuation for past and present employees. It is noted that if employers do not voluntarily disclose their historical SGC debt during the amnesty, they will face significantly higher penalties if the ATO conducts an audit. So, if you are an employer in this situation, you are best to contact your tax adviser ASAP and make arrangements to take advantage of this amnesty because it’s a once-only offer from the ATO – I doubt we’ll ever see it again.