At the time of writing this blog, most employers are actively submitting payroll events via Single Touch Payroll (STP). STP has been around since July 2018 and has now evolved into STP Phase 2. Most software companies used by small businesses to file STP reports, are now STP 2-enabled, so many employers will be reporting payroll via this mode.

While the process of filing or reporting payroll via STP is fairly straightforward, there can be occasions where things may go wrong. This is particularly true now, given the setup for STP Phase 2 is quite involved and onerous. Should the setup for STP 2 not be done correctly, this will most certainly lead to filing errors.

If a pay event is returned after filing it, the ATO will provide an error code that describes the issue. While these codes are useful in terms of helping the lodger understand what is wrong, they do not assist in providing details about how to fix the error within the software you may be using. Luckily, there is help available from each of the main software providers.

Here is a list of the software providers and the links to their help pages, should your filing return an ATO error code:

Also, from Reckon, here is a list of the most common submission errors via the ATO. Each error code is explained and a reason behind the error is given. This can be a helpful starting point when trying to rectify any STP errors.

I hope this blog has been helpful to you if you are an employer or bookkeeper. It would be a good idea to add the link for your chosen software to your favourites list for future access, should you encounter an STP filing error.

Here is a reminder that access to paid family and domestic violence leave for employees of non-small business employers (employers with 15 or more employees) began on 1st February 2023 (and 1st August 2023 for small business employers). The leave is for 10 days for any full, part-time or casual employees and is not pro-rated. Read more about this new leave type in our previous blog here.

Something important to call out in relation to paying this leave is the information that is prohibited from being included on the employee’s payslip.

Employers must not include:

A statement that an amount paid to an employee is a payment in respect of the employee’s entitlement to paid family and domestic violence leave

A statement that a period of leave taken by the employee has been taken as a period of paid family and domestic violence leave

The balance of an employee’s entitlement to paid family and domestic violence leave

The reason for not including this information is that if a perpetrator of violence gains access to the employee’s payslip and sees that this type of leave has been taken, this may pose a significant risk to the employee.

When setting up this type of leave in the payroll system, it is important to give it a generic name that does not reference the words “Family and Domestic Violence Leave”. In fact, not calling it “leave” at all is best practice. Given the payment is for an employee’s full rate of pay for the hours he/she would have worked if they weren’t on leave, then simply producing a payslip that shows “gross” pay, is recommended. In the back end of the payroll setup, details can be added noting what the payments actually are, and leave entitlement balances can be recorded but not included on the payslip (simply uncheck that box in the employee’s payroll setup (software-dependent)).

Precluding statements about this type of leave on an affected employee’s payslip is now part of the Fair Work Legislation Amendment Regulations 2022. Employers must take note and ensure that their payroll systems are set up correctly to reflect these amendments. Failing to do so may/will put affected employees at significant risk. If you are an employer, make sure you action this now (or by August 2023 if you are a small employer).

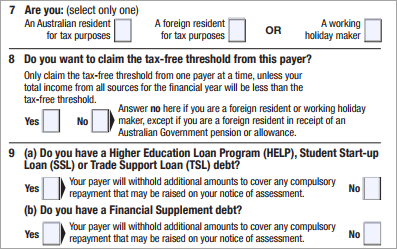

The way new employees are onboarded is changing. Currently, employers ask new employees to provide a Tax File Number Declaration form, a Super Choice form, and also other personal information required in order to set them up in their payroll systems.

While this process is fairly straightforward, often employers find themselves chasing new employees for the data and at times, needing to confirm details that may or may not be correct (usually not correct in my experience!). This process can therefore be very time-consuming and tedious for employers, not to mention that the room for error is very high. It is also not a great deal of fun for new employees either!

This is an all-in-one onboarding form that new employees access from their myGov accounts. The form will provide both the ATO and the employer with all of the information required to set up new employees in one easy action.

Importantly,this form will replace several forms. These include the Tax File Number Declaration, the Super Choice form, the Variation to Tax Withholding Declaration, the Variation to Medicare Levy Declaration, etc. Employees can also use it to update their tax circumstances, for example, if:

their residency status has changed

they no longer have a government study and training loan

they are claiming the tax-free threshold from a different employer.

This change to employee onboarding will reduce the administrative burden for employers and increase process efficiencies. It will also reduce data recording errors which are very common when obtaining personal details from new staff members.

How the new onboarding process works

Firstly, the employer needs to provide his/her ABN to the new employees.

After submitting the form, the details will be sent straight to the ATO removing the requirement for employers to send completed TFN Declarations separately. It’s important to note that the changes to Single Touch Payroll Phase 2 have also made this possible i.e. every time a pay run is reported via STP 2, employees’ tax information is sent to the ATO. Although this step can now be removed from the onboarding process, employers must continue to receive completed TFN Declarations from new employees and retain them as part of the employees’ records.

Once the form is submitted, the employee will print the form and give it to the employer who will use the information to set up the employee in the payroll system.

It’s important to note that the downloadable version of the TFN declaration form will be removed by the end of2022.

The ATO is therefore requiring new employees to be onboarded using the new above process going forward. This is a new process that both employers and employees need to understand and adopt. It has benefits in terms of efficiency and data security and in my opinion, is the way forward.

Employees (full-time, part-time, and casual), will soon be able to access 10 days of paid family and domestic violence leave in a 12-month period.

This will replace the current 5 days of unpaid leave available to affected employees.

Employees will be entitled to the full 10 days upfront, meaning they won’t have to accumulate it over time. The leave won’t accumulate from year to year if it isn’t used. The leave will renew every year on an employee’s work anniversary.

The new leave entitlement will be available from:

1 February 2023, for employees of non-small business employers (employers with 15 or more employees on 1 February 2023)

1 August 2023, for employees of small business employers (employers with less than 15 employees on 1 February 2023

Reasons for requiring this type of leave could include:

making arrangements for their safety, or the safety of a close relative (including relocation)

attending court hearings

accessing police services

attending counselling

attending appointments with medical, financial or legal professionals

An employer can ask for evidence from an employee when the leave is applied for. Types of evidence can include:

documents issued by police

documents issues by court

family violence support service documents or

statutory declaration

Employees will continue to be entitled to 5 days of unpaid family and domestic violence leave until they can access the new paid entitlement.

Reporting paid Family and Domestic Violence Leave on payslips has very specific rules – read our blog here to find out more!

As part of the set-up for STP Phase 2, employees must be labelled correctly as per a category of taxpayer (e.g. Regular, Actor, Senior or Pensioner & Horticulturist or Shearer) etc) and an additional layer known as an income type from the list below:

SAW (salary and wages)

CHP (closely held payees)

WHM (working holiday makers)

FEI (foreign employment income)

IAA (inbound assignees to Australia)

SWP (seasonal worker programs)

JPD (joint petroleum development area)

VOL (voluntary agreement)

LAB (labour hire)

OSP (other specified payments)

Most of the above income types are self-explanatory, with the exception of “closely held payees” (CHP). The CHP income type is tripping people up because they assume a payee who is a CHP should automatically be given the CHP income type. While this appears to be a logical choice, a CHP may have either an income type of SAW or CHP, depending on the entity’s situation. So how do you know when to choose one over the other? Below is my explanation of this issue.

Payroll finalisation will occur later than 14th July

Choosing either CHP or SAW Income Type

If the above reporting concessions are not being used by the entity and finalisation will occur by 14th July along with other arms-length employees, you may choose the income type CHP or SAW for your closely held payees.

I hope this has clarified the confusion around when to choose CHP as an income type for a payee who is a CHP.

If you are in the process of setting up your payroll for STP Phase 2, the ATO has a number of resources available. See also here for further ATO resources. It is worth checking them out to ensure that your setup is correct. Remember, STP Phase 2 will see a large proportion of payroll data shared with Services Australia on behalf of your employees. Services Australia will use this information as the basis for calculating future payments to your employees, should they be receiving them. For this reason, as well as ensuring employees’ wages are taxed properly, it is very important to ensure that your STP Phase 2 reporting is accurate and correct.

This excerpt is taken from the ATO website via this link.

Have you taken on new employees? Did you know they can complete a TFN declaration through ATO online services?

This is an easy way for them to provide both you and us with the information we need. If your new employee has a myGov account linked to the ATO, they can:

access ATO online services

go to the ‘Employment’ menu

select ‘New employment’ and complete the form.

This sends the TFN declaration details straight to us so you don’t have to. Your employee will need your ABN to complete the form. Once they’ve submitted the form, they need to print it and give you the summary of their tax details so you can input the data into your system.

You may be able to link your payroll software to the online commencement forms. But check first with your software provider if they offer this service.

You can also use the New employment form to collect a range of information. Despite its name, you can also use this form instead of the:

Withholding declaration form

Medicare levy variation declaration form

Superannuation standard choice form.

Your employees can use the New employment form to update their tax circumstances with you, for example, if:

their residency status has changed

they no longer have a government study and training loan

they are claiming the tax-free threshold from a different employer.

You can continue to use your current processes, including providing a paper TFN declaration where employees can’t create a myGov account or don’t have access to the internet.

STP Phase 2 is in full swing. It began on 1st January 2022 but various accounting software have not been ready until recently. This means many employers are only just now learning about, and setting up their payroll systems, to comply with STP 2 requirements.

Unfortunately, as it is still relatively new, some employers are making errors when reporting via STP Phase 2. Recently, the ATO published a list of those mistakes it is seeing. I am highlighting them here so you can be sure to avoid them when you start to report via STP Phase 2.

Common STP Phase 2 Mistakes List

Breaking the continuity of year-to-date amounts from STP 1 reporting. Unless you are using the replacing IDs methodfor transitioning to STP 2, you need to ensure that you maintain the STP 1 data that you have already reported. Your accounting solution will help you manage this and you should contact your provider if you require assistance with this issue.

Selecting “not reportable to the ATO” when setting up pay codes/categories. Most payments to employees need to be reported except for:

1. Travel allowance below the ATO’s reasonable amounts

2. Overtime meal allowance below the ATO’s reasonable amount

3. Reimbursements

4. Post-tax deductions except for those you need to separately identify.

Omitting a cessation date and reason. When an employee leaves your business, you need to report the date he finished and the reason why he left. Your accounting solution will include these fields to complete upon termination. The ATO will share this information with Services Australia which means you will no longer need to complete a separation certificate for that employee.

Some income types you report for employees will also include a special country code. If you are required to report a country code, you must report the code relevant to that employee. Some employers are incorrectly reporting a “NA” country code, thinking that it means “not applicable”. It actually means “Namibia”. So if you use NA in your reporting, you are telling the ATO that your employee is either working:

1. Overseas in Namibia or,

2. Is in Australia and they are from Namibia.

Allowances. All allowances must be reported separately using one of 8 specific allowance categories. You must not simply report an allowance to the “Other Allowance” category (allowance type OD). You must report allowances using their appropriate category because each category is treated differently for tax, super and social security purposes. Only report an amount as Allowance type OD if it’s an allowance that does not belong in one of the 8 specific allowance categories.

Treating reportable super contributions (RESC) and salary sacrifice as the same thing. These are 2 different things and need to be reported correctly. Check out this ATO video which explains how to report these payments via STP 2.

Here is the link to the ATO webpage which provides more in-depth information about the STP 2 reporting mistakes listed above, including several helpful videos.

As well as the super guarantee increase to 10.5% on 1 July 2022, employers now need to factor in a wage increase. Read more below.

National Minimum Wage Increase

The Fair Work Commission (FWC) has ordered a 5.2% wage increase to the national minimum wage (NMW). From 1 July 2022, the NMW will increase by 5.2%, which amounts to $40 a week. The new National Minimum Wage will be $812.60 per week or $21.38 per hour.

Award Minimum Wage Increase

The FWC has announced that minimum award wages will increase by 4.6%, which is subject to a minimum increase for award classifications of $40 per week and based on a 38-hour week for a full-time employee. This means minimum award wages above $869.60 per week, will get a 4.6% increase and below $869.60 per week, will get a $40 increase.

When to Apply the Increase

The new National Minimum Wage will apply from the first full pay period on or after 1 July 2022. This means if you have a weekly pay period that starts on Mondays, the new rates will apply from Monday 4 July 2022.

If you are covered by an award, award increases happen in 2 stages. Most awards will increase from the first full pay period on or after 1 July 2022 but, for some awards as listed below, the increase will happen from 1 October 2022.

Aircraft Cabin Crew Award 2020

Airline Operations – Ground Staff Award 2020

Air Pilots Award 2020

Airport Employees Award 2020

Airservices Australia Enterprise Award 2016

Alpine Resorts Award 2020

Hospitality Industry (General) Award 2020

Marine Tourism and Charter Vessels Award 2020

Registered and Licensed Clubs Award 2020

Restaurant Industry Award 2020

These awards relate to industries that are considered to be still adversely impacted by the COVID-19 pandemic.

To read more information about the wage increase go to this Fair Work web page.

In what may be just a political stunt given it’s an election year, the Victorian Government has announced that from March 2022, some casual workers will be able to claim personal leave pay. This is very unusual because casual workers are not entitled to sick leave, rather they receive a 25% loading on top of their hourly rate in lieu of holiday and sick pay. The Government is doing this to help stop the spread of COVID-19 and other diseases as it is known that casual staff will attend work when they are ill to avoid loss of wages and shifts. As per their website, their main reason for introducing this new payment is to allow casual workers to take time off if they are ill or if they need to care of family members because in their words, “no worker should have to choose between a day’s pay and their health, or the health of a loved one”. This blog will look at the details behind this scheme and ask the question, “Is this payment fair?”

What is the Victorian Sick Pay Guarantee?

The Victorian Sick Pay Guarantee (VSPG) is a government-paid initiative that allows for some casual and contract workers as listed below, to receive 38 hours of personal leave pay at the national minimum wage (currently $20.33/hour). The program will run as a trial for 2 years after which time, it may become an industry levy on employers. The scheme is active now and those wanting to apply for the leave payment can do so here.

JOB

TYPE OF WORK

Hospitality workers

Providing services to patrons of hotels, bars, cafes, restaurants, and similar venues.

Food preparation assistants

Preparing food in fast food establishments, assisting food trades workers and service staff to prepare and serve food, cleaning food preparation and service areas.

Food trades workers

Baking bread and pastry goods; preparing meat for sale; planning, organising, preparing and cooking food for dining and catering establishments.

Sales support workers

Providing assistance to retailers, wholesalers and sales staff by operating cash registers, modelling, demonstrating, selecting, buying, promoting and displaying goods.

Sales assistants

Selling goods and services directly to the public on behalf of retail and wholesale establishments.

Other labourers who work in supermarket supply chains

Including workers who fill shelves and display areas in stores and supermarkets; load and unload trucks and containers, and handle goods and freight.

Aged and disability carers

Providing general household assistance, emotional support, care and companionship for aged and disabled persons in their own homes.

Cleaners and laundry workers

Cleaning vehicles, commercial, industrial and domestic premises, construction sites and industrial machines, and clothing and other items in laundries and dry-cleaning establishments.

Security officers and guards

Providing security and investigative services to organisations and individuals, excluding armoured car escorts and private investigators.

From: https://www.vic.gov.au/sick-pay-guarantee

Is this fair for employers?

It’s important to remember that for the first 2 years, this scheme will be paid by the Government, not employers. Should it continue, however, it is believed that employers will need to pay an industry levy that will cover the VSPG for casual staff. Therefore, employment costs will increase, placing further financial pressure on employers. Employers are already paying a 25% loading on top of basic wages for casual staff which is supposed to cover their sick and holiday pay. Some would say that the addition of the VSPG is double-dipping, given that a casual worker will receive both the loading and the sick payment. If this scheme continues, some employers may be pushed to employ part-time or full-time staff only in an attempt to avoid increased costs brought on by using casual employees.

Is this fair for employees?

Certainly, it can be argued that casual employees are an “at-risk” demographic. They are subject to reduced hours, unstable employment and increased difficulty in maintaining a robust credit record. They do not have the same job security as their part or full-time counterparts. As they generally do not work full-time hours, their income is greatly reduced and even though they are in receipt of the 25% loading, they do not have the ability to save this loading for sick days, as they need every cent just to live! Many are working paycheck to paycheck in order to pay rent and put food on the table. This being the case, it is understandable that some would choose to go to work sick, rather than lose wages, shifts and/or their job. With this in mind, the VSPG is fair for these employees. They can maintain their income and avoid spreading viruses like COVID-19. This is good for everyone.

Here’s what I think

I do like the idea of the VSPG. I am sure it will really help many casual workers (double-dipping or not). However, I think it’s just a temporary solution because once the VSPG payment is used up (the 38 hours), it is likely that workers will go back to attending work when they are ill. I’ve had a think about it and here are some alternative solutions I’ve come up with. Casual workers could:

Opt-in for loading or leave accruals, but not both.

Receive a smaller loading and accrue leave as well.

Apply for a top-up payment from the Government, when wages fall below a certain point for a particular period.

These are just some ideas jumping around in my head, but as I write this, I am left wondering if the double-dipping issue is the real problem here. Perhaps the real issue is not what is paid to casual staff, but rather, how much.

I believe, underlying the need to top up casuals’ pay with the VSPG and/or loadings, is a wage level problem. If these employees were paid adequately in the first place, then perhaps there would be no need for either the loading or the VSPG.

For many casual employees, wages are just too low, loading or no loading. Many who are students, carers or parents cannot work full-time hours and, as such, are subject to very low incomes. In my opinion, we need to look at wage growth and inflation before offering bandaid solutions such as the VSPG. Wages need to be kept in line with inflation. Simple as that. The Government that makes this happen, will get my vote this election year. Sadly, I think I’ll be left wanting…

As you probably know by now, STP Phase 2 has begun. It began on 1st January 2022, with a deferred hard start date by the ATO of 1st March 2022.

Your payroll software provider may have a deferral in place with the ATO for a later start date (see list below) which will cover you as their customer. However, some software providers are ready now and do not have a deferral in place. Examples of these are Quickbooks Online (KeyPay) and Saasu. If you are using one of this software or something else, then your business should be ready for STP 2 and be reporting data to the ATO as per their requirements. (Note, to check if your software is STP 2 enabled, you can go to this ATO page and search for “Payroll Event 2020”. This will produce a list of software that is STP 2 – ready.)

If you know you are not ready and need more time, you can try to apply to the ATO for a deferral. You can do this via Online Services for Business. Simply log in and follow these steps:

1. Select Employees 2. Select STP deferrals and exemptions 3. Select Delayed transition to STP Phase 2 expansion 4. Complete the request 5. Click Submit.

You will also need to advise: 1. Which payroll software is being used; 2. The reason a delay is being sought, and 3. The expected date the business will be able to start reporting under STP 2.

Software Providers with a Current STP 2 Deferral The following SPs have a current deferral in place with the ATO which also covers you, as their customer: