If your business has a tax debt of at least $100K and it is overdue by more than 90 days, chances are you will soon receive a letter from the ATO explaining its intention to report the debt to credit reporting agencies. These letters are known as “Notices of Intent to Disclose”.

See below for the tax ruling background.

If your tax debt is reported to such credit agencies, this would have a detrimental effect on the business’s ability to maintain a good credit rating or score, leading to a possible inability to lend from banks and finance companies and/or obtain extended payment terms (credit) from suppliers.

The Notice of Intent to Disclose letter will outline ways to avoid reporting action, including paying out the debt, entering into a payment plan and several other methods. It is important to note that where exceptional circumstances have led to, and/or impacted the tax debt, such as family tragedy, serious illness and/or natural disasters, it may be possible to prevent tax debt reporting.

If you think your business may be in the firing line for receipt of one of these letters from the ATO, it would be prudent to contact your tax agent ASAP to discuss the way forward.

(The measure is known as “Disclosure of Business Tax Debt”, and received Royal Assent on 28th October 2019. This measure can be sourced in Schedule 5 of the Treasury Laws Amendment (2019 Tax Integrity and Other Measures No. 1)).

In what may be just a political stunt given it’s an election year, the Victorian Government has announced that from March 2022, some casual workers will be able to claim personal leave pay. This is very unusual because casual workers are not entitled to sick leave, rather they receive a 25% loading on top of their hourly rate in lieu of holiday and sick pay. The Government is doing this to help stop the spread of COVID-19 and other diseases as it is known that casual staff will attend work when they are ill to avoid loss of wages and shifts. As per their website, their main reason for introducing this new payment is to allow casual workers to take time off if they are ill or if they need to care of family members because in their words, “no worker should have to choose between a day’s pay and their health, or the health of a loved one”. This blog will look at the details behind this scheme and ask the question, “Is this payment fair?”

What is the Victorian Sick Pay Guarantee?

The Victorian Sick Pay Guarantee (VSPG) is a government-paid initiative that allows for some casual and contract workers as listed below, to receive 38 hours of personal leave pay at the national minimum wage (currently $20.33/hour). The program will run as a trial for 2 years after which time, it may become an industry levy on employers. The scheme is active now and those wanting to apply for the leave payment can do so here.

JOB

TYPE OF WORK

Hospitality workers

Providing services to patrons of hotels, bars, cafes, restaurants, and similar venues.

Food preparation assistants

Preparing food in fast food establishments, assisting food trades workers and service staff to prepare and serve food, cleaning food preparation and service areas.

Food trades workers

Baking bread and pastry goods; preparing meat for sale; planning, organising, preparing and cooking food for dining and catering establishments.

Sales support workers

Providing assistance to retailers, wholesalers and sales staff by operating cash registers, modelling, demonstrating, selecting, buying, promoting and displaying goods.

Sales assistants

Selling goods and services directly to the public on behalf of retail and wholesale establishments.

Other labourers who work in supermarket supply chains

Including workers who fill shelves and display areas in stores and supermarkets; load and unload trucks and containers, and handle goods and freight.

Aged and disability carers

Providing general household assistance, emotional support, care and companionship for aged and disabled persons in their own homes.

Cleaners and laundry workers

Cleaning vehicles, commercial, industrial and domestic premises, construction sites and industrial machines, and clothing and other items in laundries and dry-cleaning establishments.

Security officers and guards

Providing security and investigative services to organisations and individuals, excluding armoured car escorts and private investigators.

From: https://www.vic.gov.au/sick-pay-guarantee

Is this fair for employers?

It’s important to remember that for the first 2 years, this scheme will be paid by the Government, not employers. Should it continue, however, it is believed that employers will need to pay an industry levy that will cover the VSPG for casual staff. Therefore, employment costs will increase, placing further financial pressure on employers. Employers are already paying a 25% loading on top of basic wages for casual staff which is supposed to cover their sick and holiday pay. Some would say that the addition of the VSPG is double-dipping, given that a casual worker will receive both the loading and the sick payment. If this scheme continues, some employers may be pushed to employ part-time or full-time staff only in an attempt to avoid increased costs brought on by using casual employees.

Is this fair for employees?

Certainly, it can be argued that casual employees are an “at-risk” demographic. They are subject to reduced hours, unstable employment and increased difficulty in maintaining a robust credit record. They do not have the same job security as their part or full-time counterparts. As they generally do not work full-time hours, their income is greatly reduced and even though they are in receipt of the 25% loading, they do not have the ability to save this loading for sick days, as they need every cent just to live! Many are working paycheck to paycheck in order to pay rent and put food on the table. This being the case, it is understandable that some would choose to go to work sick, rather than lose wages, shifts and/or their job. With this in mind, the VSPG is fair for these employees. They can maintain their income and avoid spreading viruses like COVID-19. This is good for everyone.

Here’s what I think

I do like the idea of the VSPG. I am sure it will really help many casual workers (double-dipping or not). However, I think it’s just a temporary solution because once the VSPG payment is used up (the 38 hours), it is likely that workers will go back to attending work when they are ill. I’ve had a think about it and here are some alternative solutions I’ve come up with. Casual workers could:

Opt-in for loading or leave accruals, but not both.

Receive a smaller loading and accrue leave as well.

Apply for a top-up payment from the Government, when wages fall below a certain point for a particular period.

These are just some ideas jumping around in my head, but as I write this, I am left wondering if the double-dipping issue is the real problem here. Perhaps the real issue is not what is paid to casual staff, but rather, how much.

I believe, underlying the need to top up casuals’ pay with the VSPG and/or loadings, is a wage level problem. If these employees were paid adequately in the first place, then perhaps there would be no need for either the loading or the VSPG.

For many casual employees, wages are just too low, loading or no loading. Many who are students, carers or parents cannot work full-time hours and, as such, are subject to very low incomes. In my opinion, we need to look at wage growth and inflation before offering bandaid solutions such as the VSPG. Wages need to be kept in line with inflation. Simple as that. The Government that makes this happen, will get my vote this election year. Sadly, I think I’ll be left wanting…

As you probably know by now, STP Phase 2 has begun. It began on 1st January 2022, with a deferred hard start date by the ATO of 1st March 2022.

Your payroll software provider may have a deferral in place with the ATO for a later start date (see list below) which will cover you as their customer. However, some software providers are ready now and do not have a deferral in place. Examples of these are Quickbooks Online (KeyPay) and Saasu. If you are using one of this software or something else, then your business should be ready for STP 2 and be reporting data to the ATO as per their requirements. (Note, to check if your software is STP 2 enabled, you can go to this ATO page and search for “Payroll Event 2020”. This will produce a list of software that is STP 2 – ready.)

If you know you are not ready and need more time, you can try to apply to the ATO for a deferral. You can do this via Online Services for Business. Simply log in and follow these steps:

1. Select Employees 2. Select STP deferrals and exemptions 3. Select Delayed transition to STP Phase 2 expansion 4. Complete the request 5. Click Submit.

You will also need to advise: 1. Which payroll software is being used; 2. The reason a delay is being sought, and 3. The expected date the business will be able to start reporting under STP 2.

Software Providers with a Current STP 2 Deferral The following SPs have a current deferral in place with the ATO which also covers you, as their customer:

As part of the Government’s Treasury Laws Amendment Bill 2021 which passed on 12th February 2022, it has been decided that the $450 superannuation guarantee threshold will be removed. This will begin on July 1, 2022.

The scrapping of the threshold will make about 300,000 more workers eligible for super contributions, including many low-income employees in part-time and casual positions. This will ensure all workers can build their retirement savings, not just those in higher-paid, full-time positions.

Currently, employees must gross a minimum of $450 per month with one employer in order to be paid super on top of those wages (note, this can be $350 per month for those working in the hospitality industry e.g. award MA000009 Hospitality Industry). Those who work casually or part-time may find that they never quite reach that threshold even if they hold several jobs at once. For example, an employee who has 3 casual jobs, earning $300 per job per month, will not receive super on any of those wages due to the $450 threshold. This hardly seems fair and is the main driver for the removal of the threshold.

So, from July 1, 2022, if you employ staff, you will need to pay super contributions on all their earnings, no matter how little each month. For example, if your employee grosses $100 for the month, then super of $10 (currently paid at 10%) will accrue and be paid to the employee’s super fund.

While the move to remove the super threshold is pleasing in my opinion, it is worth noting that employers’ payroll budgets will increase as a result. The cost to employ staff is currently very high and this change will only serve to make it higher! Add in the next super guarantee increase to 10.5%, also from 1 July 2022, and I think we shall see some employers squirming!

While your payroll software will more than likely be upgraded to take up the removal of the super threshold, it is worth noting the start date to ensure you can check your payroll setup is correct when the time comes.

As per Fair Work, some employees will be entitled to unpaid pandemic leave from 31 December 2021 to 30 June 2022. This affects 74 awards – see this list to check if your workplace is affected.

But what is unpaid pandemic leave and how should it be used?

What is unpaid pandemic leave?

If an employee is prevented from working because he has to self-isolate as directed by:

government or medical authorities or his doctor, or by

enforceable government directions placing restrictions on non-essential businesses,

he will be eligible for up to 2 weeks’ unpaid pandemic leave.

What do I need to know about unpaid pandemic leave?

Full-time, part-time and casual staff are eligible.

Paid leave does not have to be used before pandemic leave is taken.

All staff can take the 2 whole 2 weeks leave - it is not pro-rated for staff who do not work full-time.

Unpaid pandemic leave does not affect other types of leave, paid or unpaid.

My employee wants to take unpaid pandemic leave. What should I do?

Your employee needs to advise you when they will take the leave (even if it’s already started) and the reason they are taking it. He should do this via email so that you both have written evidence as to when the leave was taken. The employee should indicate how long he will be absent from work. You can ask your employee to provide evidence that shows why they took the leave, such as a medical certificate. Note, if your employee is actually ill from Covid-19, then he/she may benefit from taking paid personal leave instead. In this case, you could ask for other evidence such as a positive PCR or a Rapid Antigen Test reading.

This is the final blog in a four-part blog series about STP Phase 2. In part one of this blog series, we looked at the benefits of phase 2, then, in part two, we outlined which software providers are ready for STP 2 now. Part three in the series delved deeper into the technical side of STP Phase 2. This final blog will focus on the sorts of things employers or their bookkeepers can do now, in order to plan ahead for a smooth transition to STP Phase 2.

The best thing you can do is to start to review your current payroll setup. Check employees’ details both personal and payroll-related. I have created a spreadsheet you can use to review your current employees/payees which you can download and use as needed (see below). This spreadsheet will collate most of the information you will need in order to transition to STP 2. Start the process by completing the spreadsheet and then, when you are ready to transition, you will have most of the required information at your fingertips.

Next, sit down with your employees/payees and explain what will happen once STP 2 begins. Tell them about how their information will be shared with the ATO and Services Australia. Explain that their payslips and income statements will look different and why. You may need to ask payees for more personal information during the setup of STP 2 – try to get ahead of the game and find out what sorts of data you don’t have and work with your payees to obtain it.

Keep an eye on your payroll provider’s pathway to STP 2. Your provider will advise you when you can transition and how it is to be done within the software itself. This may not happen for some months, but you can still prepare as per my above tips!

Lastly, think about when you would like to transition to STP 2. Yes, there are time constraints as per the ATO but they do say you can move over at any time during the year (provided you are covered by a deferral). However, you may like to put a plan in place and decide on a cutover date. That way, you can work towards the move to STP 2 in a timely manner and in a fashion that works for you and your business.

Lastly, to help you with your STP 2 plan and research, the ATO has created a set of guidelines for employers (see below). Download it and pop it away for use when you are ready to transition (or start your research now). Remember, don’t panic! There’s plenty of time and there will be a lot of help available to you when the time comes to tackle STP Phase 2!

How payroll is changing and what it will look like - getting technical!

What is STP Phase 2?

Basically, STP Phase 2 is the same as STP Phase 1 except that more payroll data now needs to be reported. STP 2 requires drilling down into the details about your payees, their payments, PAYG withheld, and superannuation. These extra details will be shared with the ATO and Services Australia, providing them with greater visibility about your payees and you, as an employer.

While the overall process of transferring your payroll data to the ATO via STP is not changing, there are some specific attributes of the process that will change. These are listed below:

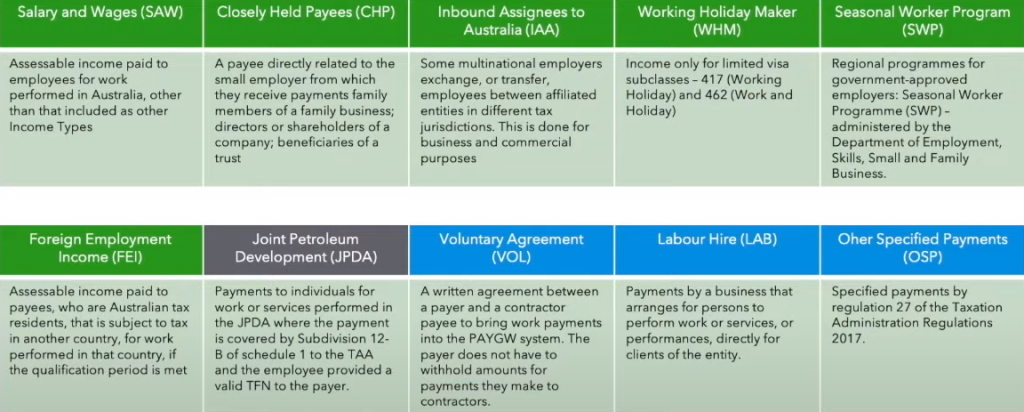

Reporting of income types and country codes - see graphic below.

Disaggregation of gross income - you will be required to report more detail about income including gross, allowances, paid leave, overtime, bonuses and commissions, directors' fees and salary sacrifice.

New fields to replace Tax File Number Declaration services - while you will still need to retain a copy of the employee's TFND, you will no longer be required to send a copy to the ATO as data relating to the TFND will be transmitted at each and every pay event.

Lump Sum E by financial year - If you need to make a Lump Sum E payment (back payments more than 12 months old), you won't need to provide a Lump Sum E letter to your employee as it will be included in the STP report.

Adding new cessation type reason - because the date and reason for employment cessation will be in the STP report, you will no longer need to complete and provide separation certificates to employees.

New Child Support Agency deduction and garnishee – Child Support deductions and/or garnishees will be reported via STP reducing the need for you to send separate remittance advice to the Child Support Registrar.

Transferring payee year-to-date amounts – if you change software type or an employee's payroll ID number, this will be reported via the STP report. This will help avoid duplicate income statements appearing in employees' myGov accounts.

Separately reporting salary sacrifice - you will be required to report the pre-sacrificed income as well as the amount of salary sacrifice.

Our main message to you is “do not panic”! Your software provider will assist you with the move to STP 2 when the time comes. In the meantime, we suggest that you do some research to assist you in better understanding how your payroll will be affected by STP Phase 2. To help you with this, we have created the below table. There are links to relevant ATO web pages which will provide specific information about how STP 2 relates to your employees, their payments, and tax withheld from those payments.

STP Phase 2 has started! It began on 1st January 2022 and if you are ready and your software is ready, you can begin to report your payroll via this next stage of STP now!

If you aren’t ready, don’t worry, the ATO has provided a blanket deferral to the 1st March 2022. This means that if your software is ready now, you have until 01/03/22 to ensure you are organised and have updated your payroll data to enable a smooth transition to STP Phase 2 reporting.

But how do you know if your software is ready? Most providers would have contacted you by now to explain their plans, but in case you missed their emails, here is a summary of the main providers and whether or not they are ready now:

Have you heard? STP (Single Touch Payroll) is expanding from Phase 1 to, you guessed it, Phase 2. For those who don’t know, STP is a technology that automates the transfer of payroll data from payroll software to government departments, mainly the ATO. STP Phase 2 will see payroll data also being shared with Services Australia, the first in a long list of government departments who will eventually get to see your payroll information (in my opinion). The expansion plan also means that employers will need to update their payroll systems in order to provide much more detail about their payroll at each payroll event (more about that in coming blogs).

This compliance change is happening for better or for worse, so my question is “STP Phase 2, what is it good for?” Absolutely nothing! No, only joking! It turns out that there are quite a few benefits for both employers and employees. This blog will outline those benefits.

Benefits for Employers

Tax File Number Declarations - although you will need to keep copies of your employees' TFN Declarations as part of your employee records, you will no longer need to send them to the ATO. This is because the information will be sent via each pay event through STP.

By nominating an "income type" for employees, you can tell the ATO if you're using concessional reporting for closely held payees or inbound assignees.

If you need to make a Lump Sum E payment (back payments more than 12 months old), you won't need to provide a Lump Sum E letter to your employee as it will be included in the STP report.

If you change software type or an employee's payroll ID number, this will be reported via the STP report. This will help avoid duplicate income statements appearing in employees' myGov accounts.

Data will be shared about some employees with Services Australia (SA). This means that information SA requires from you will be easier to provide e.g. payslips for prior periods.

Because the date and reason for employment cessation will be in the STP report, you will no longer need to complete and provide separation certificates to employees.

Child support deductions and/or garnishees will be reported via STP reducing the need for you to send separate remittance advice to the Child Support Registrar.

Benefits for Employees

Income statements will become more accurate because the ATO will have better visibility of the types of income an employee receives.

If an employee makes an error such as failing to report that he has a study loan debt (resulting in an unwanted tax bill), the ATO will be better placed to rectify the issue sooner rather than later.

If employees have dealings with Services Australia (SA), they will see a more streamlined approach to data capture evolve over time, including:

Prefilled details on claim forms and fewer requests for documentation;

Spending less time on the phone to SA to confirm details;

Receiving SMS or email advice when STP data shows their family income estimate may be too low, they have a new job or their employment details have changed in some way;

Ensuring that they are paid the correct amount from SA, and

Helping SA understand their financial situation if employees need to repay a debt to SA.

STP Phase 2 requires employers and bookkeepers to make major changes to payroll set up which in the interim, may seem onerous and pretty annoying. However, as can be seen above, there are many benefits for both employers and employees that will come from STP Phase 2 in the long run.

Of course, time will tell if these changes will run smoothly or have unwanted side effects. We will all have to wait and see how things play out. In the meantime, for those wanting further information about STP Phase 2, please visit the ATO STP Phase 2 resources page.

Finally, after the dark days of COVID-19 and endless lockdowns, etc., we are now seeing glimpses of opportunities to travel again (THANK GOD!). For business owners, this means work-related travel is once more on the table. Given it’s been a while between trips, I thought it might be useful to provide a refresher on travel diaries and when they are required.

When do I need to keep a travel diary and what do I record?

When you travel for work or your business, you are sometimes required to keep a travel diary as per the ATO to assist in working out which part of your travel is tax-deductible. I have outlined the circumstances below which would dictate when you should keep such a diary:

You are travelling for 6 or more nights in a rowoutside of Australia, regardless of whether or not the amount you are claiming exceeds the reasonable travel allowance amount.

You are travelling in Australia (more than 6 nights in a row) and the amount you want to claim is more than the reasonable travel allowance amount.

You should include the following in the diary:

Your location

The nature of the activity e.g. a conference

The day/s and time/s (start and end times)

The length of the activity e.g. 2 days

When you stopped for meals

Travel movements and activities before the activities end, or as soon as possible afterwards

The entries must be in English

What can I use as my travel diary?

The ATO has said that you can use a diary or journal of your choice for the purposes of keeping a travel diary. You can also use your digital calendar as well, making sure to attach receipts/invoices to each entry.

What other records do I need to keep?

It goes without saying, that you should keep all receipts and invoices related to your travel as well as the travel diary. This will make both the bookkeeper’s and tax agent’s jobs much easier 🙂 and make the ATO very happy!

Lastly, you need to remember that if you were required to keep a travel diary and you didn’t, then you may not be able to claim the relevant travel expenses on your tax return! Speak to your tax agent for further advice if this affects you.