Travel Diaries

Finally, after the dark days of COVID-19 and endless lockdowns, etc., we are now seeing glimpses of opportunities to travel again (THANK GOD!). For business owners, this means work-related travel is once more on the table. Given it’s been a while between trips, I thought it might be useful to provide a refresher on travel diaries and when they are required.

When do I need to keep a travel diary and what do I record?

When you travel for work or your business, you are sometimes required to keep a travel diary as per the ATO to assist in working out which part of your travel is tax-deductible. I have outlined the circumstances below which would dictate when you should keep such a diary:

You are travelling for 6 or more nights in a row outside of Australia, regardless of whether or not the amount you are claiming exceeds the reasonable travel allowance amount.You do not receive a travel allowance,You are travelling in Australia (more than 6 nights in a row) and the amount you want to claim is more than the reasonable travel allowance amount.

You should include the following in the diary:

Your locationThe nature of the activity e.g. a conferenceThe day/s and time/s (start and end times)The length of the activity e.g. 2 daysWhen you stopped for mealsTravel movements and activities before the activities end, or as soon as possible afterwardsThe entries must be in English

What can I use as my travel diary?

The ATO has said that you can use a diary or journal of your choice for the purposes of keeping a travel diary. You can also use your digital calendar as well, making sure to attach receipts/invoices to each entry.

What other records do I need to keep?

It goes without saying, that you should keep all receipts and invoices related to your travel as well as the travel diary. This will make both the bookkeeper’s and tax agent’s jobs much easier 🙂 and make the ATO very happy!

Lastly, you need to remember that if you were required to keep a travel diary and you didn’t, then you may not be able to claim the relevant travel expenses on your tax return! Speak to your tax agent for further advice if this affects you.

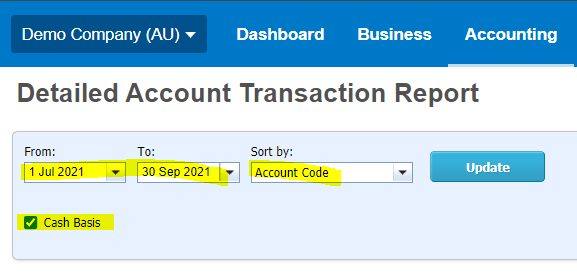

so you can find it easily when you do your next BAS.

so you can find it easily when you do your next BAS.